Let’s not sugar coat it – each year we pay large sums in taxes (some more than others depending on what you earn…. AND what you can claim).

You earnt it, so we want to help you keep it (well, as much of it as possible). Ultimately, that comes down to knowing what you can and should be claiming, and that’s where we come in. We’ve been doing this for over 20 years and would love to use our experience to maximise your tax return this tax time.

Our “Let’s do the maths” series highlights some different scenarios that ultimately will have an impact on your back pocket. We’ll have new tax tips and tax advice for you each week on our social channels, so stay tuned!

Tax Tip 1: Private Health vs No Private Health

Depending on what you earn, having (or not having) private health can impact how much extra you pay in taxes. As an Australian resident for tax purposes you are subject to the Medicare levy. The Medicare levy is in addition to the tax you pay on your taxable income, unless you qualify for a reduction or exemption. In addition to the Medicare levy, you may have to pay the Medicare levy surcharge (MLS) if:

- you, your spouse or dependant children don’t have an appropriate level of private patient hospital cover, and

- your income is above $90,000 for singles and $180,000 (plus $1,500 for each dependent child after the first one) for families.

**We’ve done a quick example equation, but to work out how private health vs no private health impacts you, you can find a handy calculator on the ATO website.

Let’s do the maths!

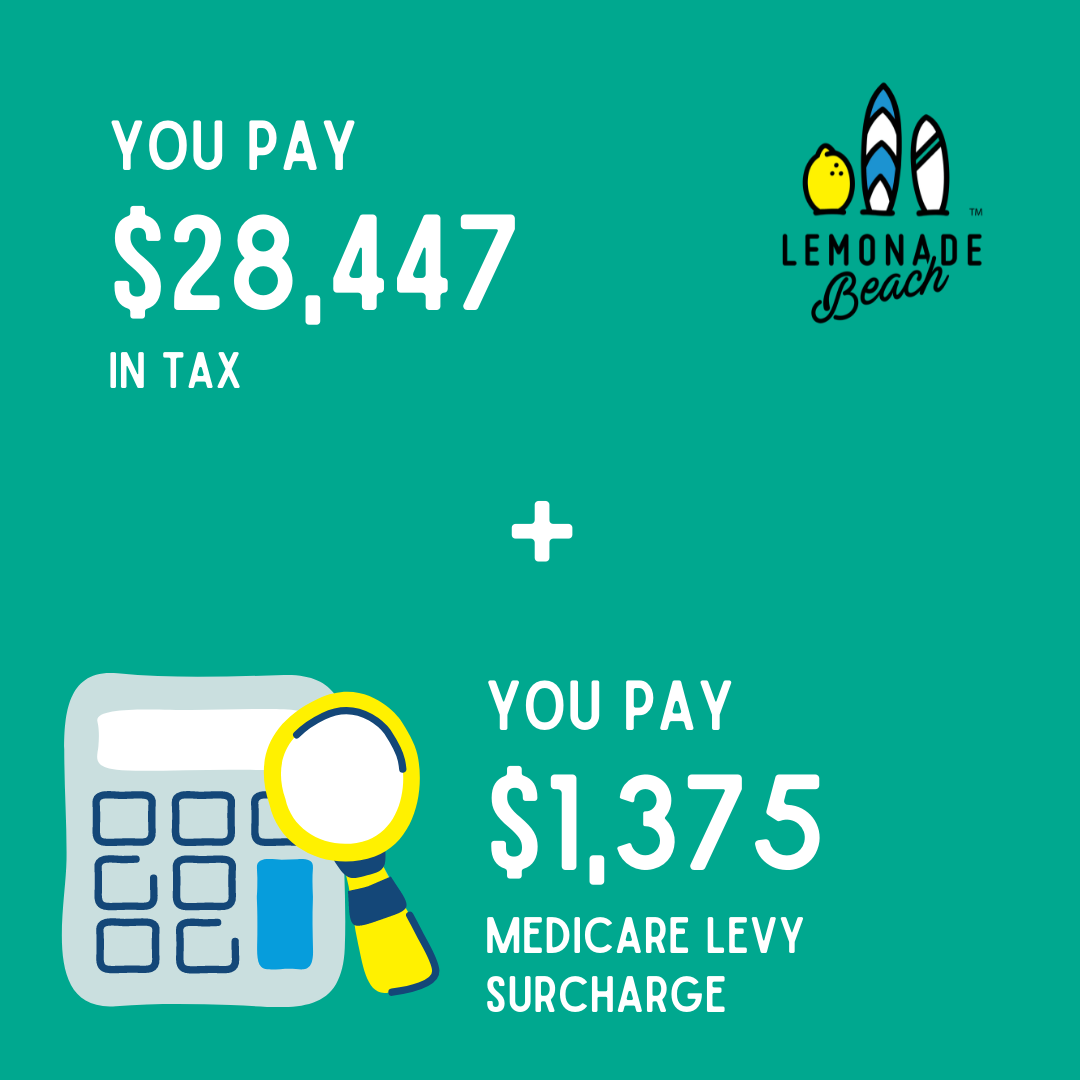

Tim and Tara both work for the same employer, they both are on a salary of $115,000 pa. Neither of them has a spouse or children. They both have similar tax deductions of $5,000 per year. Tara has the required level of private health insurance to cover her as a private patient in hospital and has held it for the whole year, Tim doesn’t have any private health insurance. Based on their taxable incomes of $110k ($115k – 5k). Tim and Tara will each pay $28,447 tax for the 2022 Financial Year (including the 2% medicare levy). As Tim doesn’t have private health insurance, he will also need to pay the Medicare Levy Surcharge. Based on his adjusted taxable income of $110k – Tim will need to pay an additional 1.25% or $1,375.

Tax Tip 2: The impact of additional Superannuation contributions

Making additional contributions into your super is just one of the ways you can reduce the amount you pay on tax. However, keep in mind that there’s a limit to how much extra you can contribute. The combined total of your employer and salary sacrificed contributions must not be more than $27,500 per financial year.

If you earn over $37,000 per year, it may be beneficial to explore extra super contributions.

We’ve done a quick example equation to illustrate how making extra super contributions can impact the tax you pay.

Let’s do the maths!

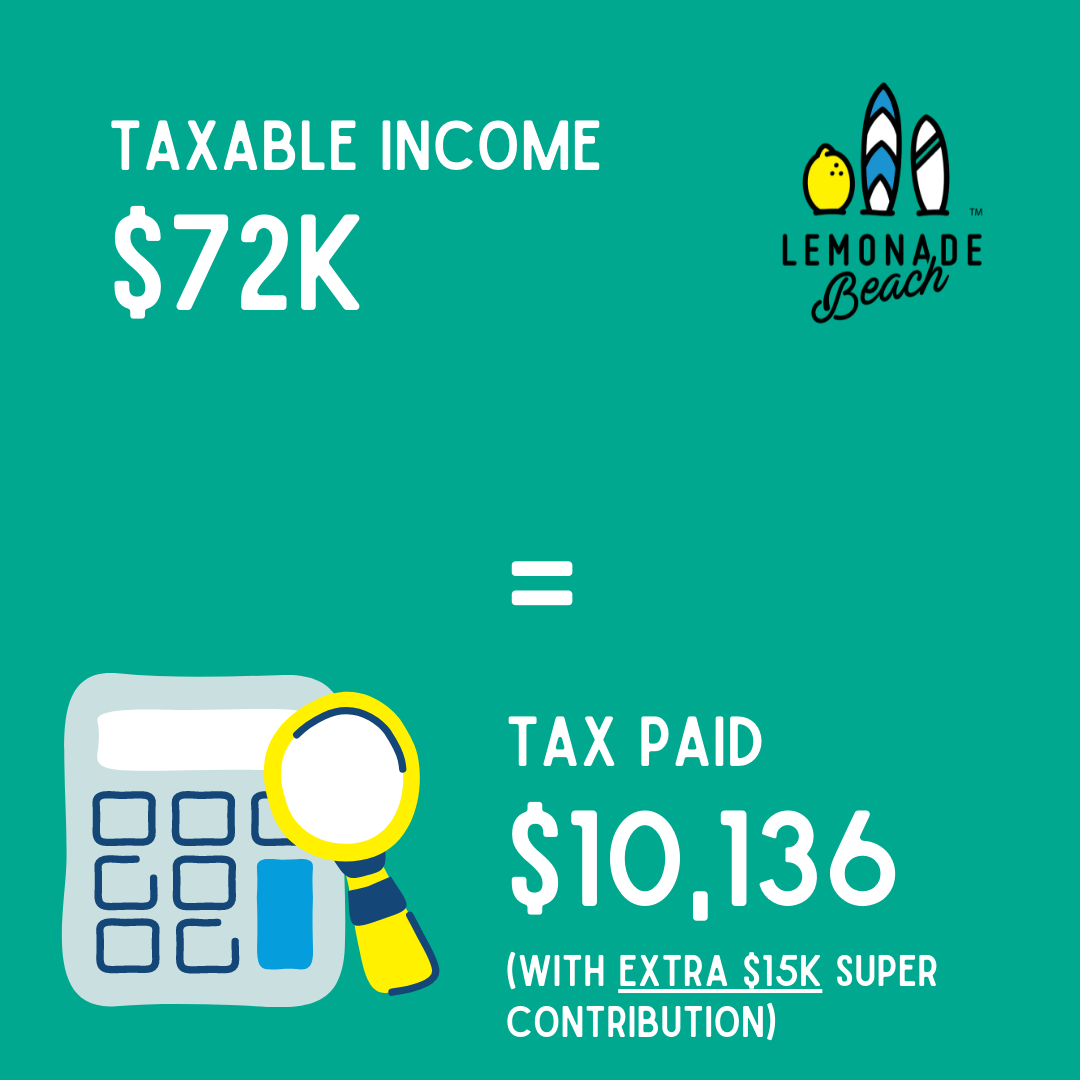

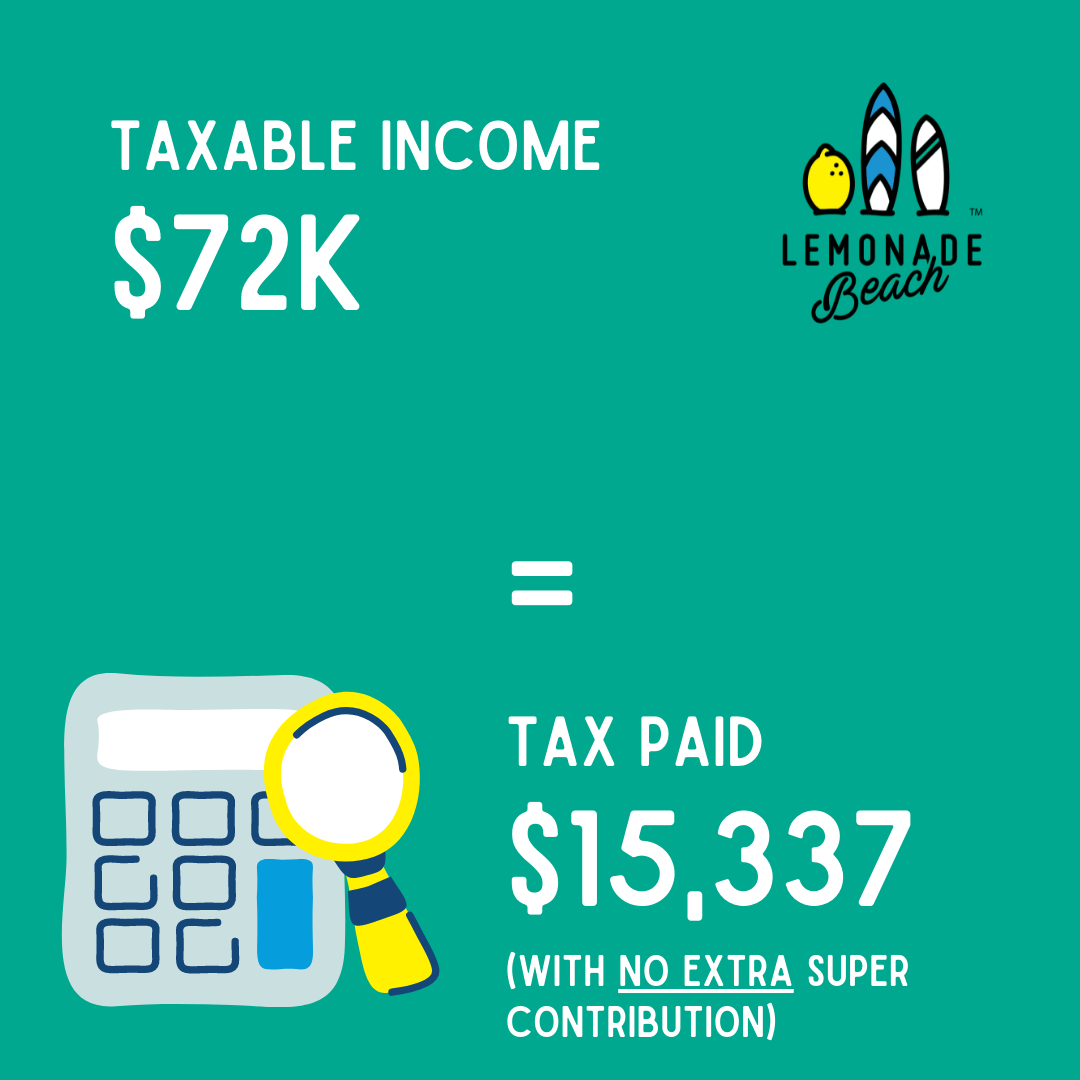

Jamie receives a salary of $75,000 with tax deductions of $3,000 – leaving taxable income of $72,000.

She would ordinarily pay tax (including medicare levy) of $15,337 on this income.

During the 2022 financial year she would like to boost her superannuation. Her employer has already contributed 7.5k for the year leaving 20k of her cap remaining. She decides to contribute an extra 15k and ensures this is paid to her fund by their 2022 cut off date. She also informs her fund that she wants to claim a tax deduction for it.

This reduces her taxable income to $57,000 and reduces the tax paid for the year to $10,136. Effectively saving Jamie $5,201 of tax.

Tax Tip 3: Cents per km Claim vs Log Book Claim

There are two methods that individuals can use to claim motor vehicle expenses in their tax return.

- Cents per km method – Limited to 5,000km

- Log book method – requires a valid log book for minimum 12 weeks

Let’s do the maths!

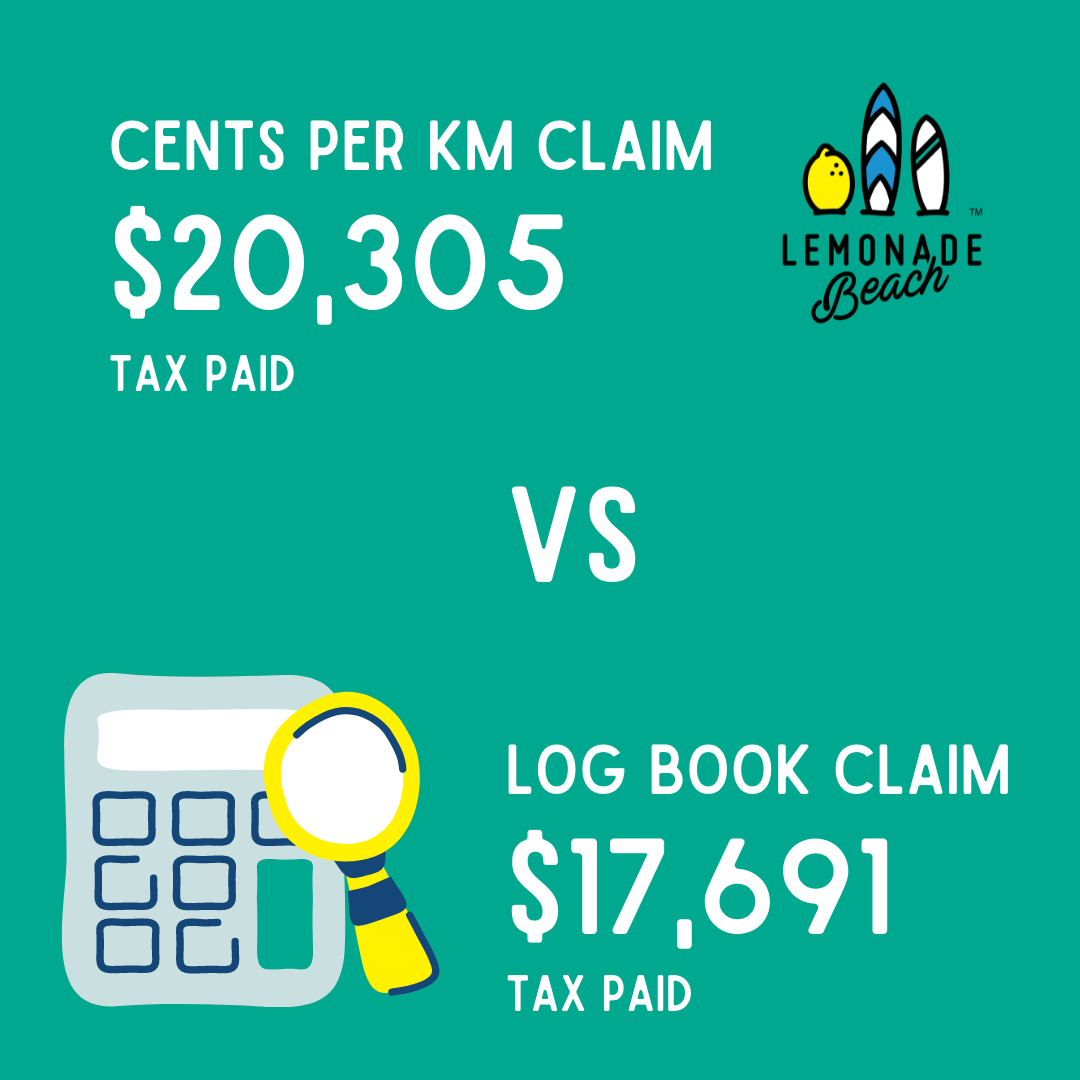

Susan and Sally are both sales reps for a homewares wholesaler. They both earned a similar income of $90,000 (including commissions) for the 2022 financial year. Their employment duties require them to attend trade shows as well as visit stockists and they use their own vehicles to carry out these duties. They both purchased new vehicles in June 2021 for $30,000.

From Sally’s odometer readings she drove 25,000km during the year, and she estimates that at least 80% of this would be for work. However, she doesn’t have a valid logbook, so is limited to claiming 5000km at $0.72 per km or $3,600 deduction.

This reduces her taxable income to $86,400 – and she pays a total of $20,305 tax for the year.

Susan kept a logbook for her car when she purchased it and her usage of the vehicle hasn’t changed since. Her logbook shows that her business use of the car is 76%.

Her costs of running the vehicle for the year are:

- Insurance$935

- Registration $784

- Servicing $368

- Fuel $3640

She also has a loan on the vehicle and paid $1480 in interest.

She can also claim depreciation on the vehicle at 25% diminishing value or $7,500 for the year.

Her total costs are $14,707 of which she can claim her log book % of 76% or $11,177

This reduces her taxable income to $78,823 – and she pays a total of $17,691 tax for the year.

Susan paid $2,614 less tax than Sally simply because she kept a log book and motor vehicle records.

More information about the deductions you can claim for Transport and Travel can be found on the ATO website.

Tax Tip 4: Temporary Full Expensing

How can the government’s introduction of Temporary Full Expensing impact the amount you pay in tax?

Let’s do the maths!

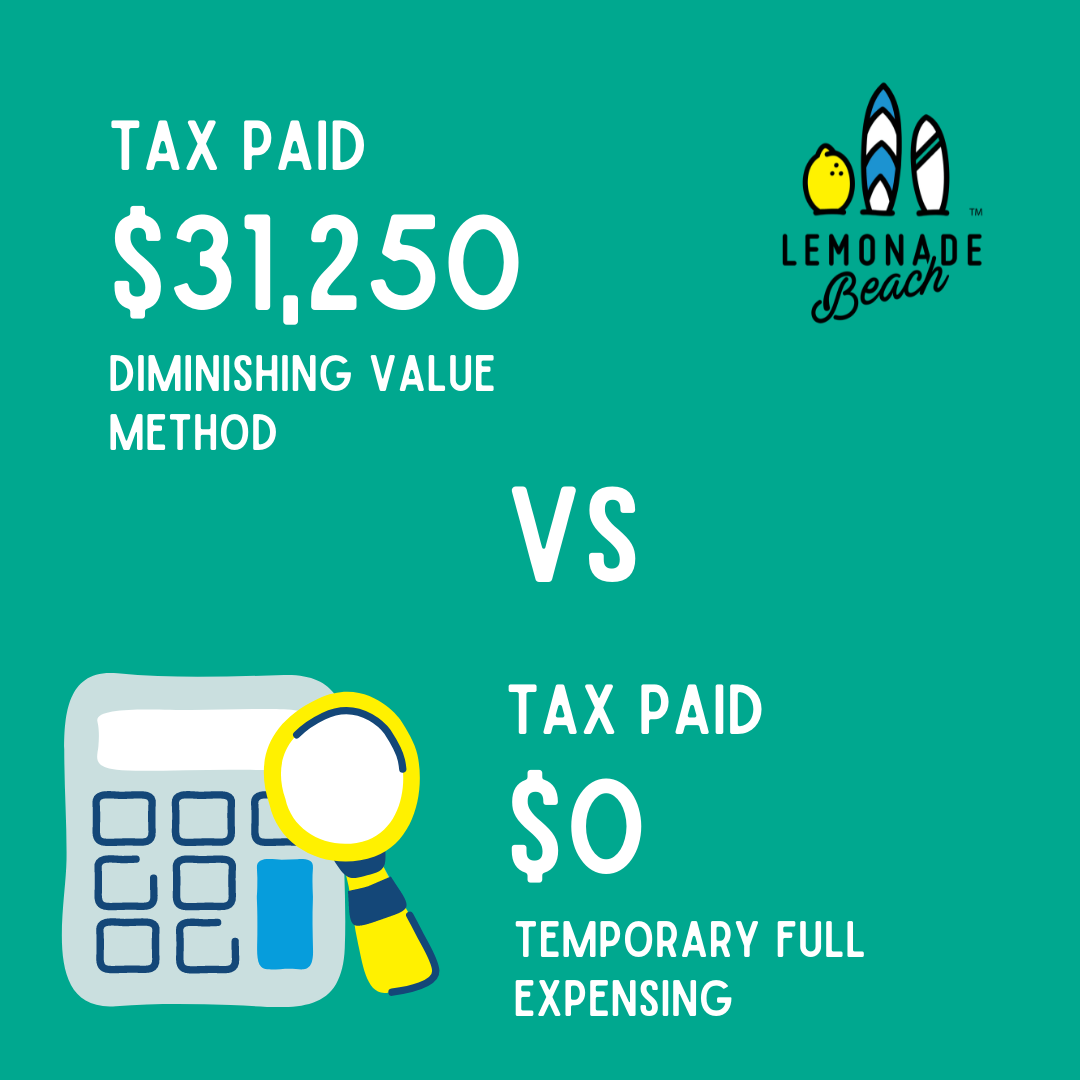

John owns and operates a small building company through his company. 2022 has been a good year and John decided early on to upgrade some of the equipment in the business. Altogether the company purchased 350k of new equipment using a combination of cash and equipment finance and all the items have been received and used in the business before 30 June 2022.

The company’s profit before depreciation in 2022 is $200k.

Normally, all the equipment items purchased would be depreciated over 10 years using the Diminishing Value Method – this would mean the company would be able to claim a tax deduction of $75,000 for depreciation in the 2022 Financial year, reducing the profit to $125,000. And the company would pay tax at 25% or $31,250.

However due to the Temporary Full Expensing measures introduced during covid, John’s company is able to claim a full deduction for the new equipment. This reduces the Company’s profit from 200k to a Loss of $150k – as such the company doesn’t have to pay any tax for the year.

Tax Tip 5: Loss Carry-Back

How can the government’s introduction of Loss Carry-Back rules impact the amount you pay in tax?

Let’s do the maths!

Using our previous example, John’s building company makes a taxable loss of $150k for the 2022 financial year (due to temporary full expensing).

John’s company has been operating for three years and has made the following historical profits:

- 2019 $180,000 – tax paid $49,500

- 2020 $170,000 – tax paid $46,750

- 2021 $220,000 – tax paid $57,200

All the tax has been paid and to date the company hasn’t declared any dividend. At 30 June 2022 the franking account balance is in credit of $153,450.

The company’s tax rate for 2022 is 25%.

Normally a company has to carry forward losses to offset future profits, however due to covid, the government introduced Loss Carry Back rules. John elects to use these rules and carry the 150k loss backwards against 2019 year profits. His accountant fills out the relevant section on his company tax return and John claims back $37,500 in tax previously paid (150k * 25%) and gets a refund from the ATO for this amount.

His accountant also reduces the company’s franking account by the tax refunded, or $37,500.

*Note Loss Carry Back only applies to company structures

Need some help this tax time? Please Contact Us to discuss more.