It is common for owners (shareholders) of companies to want to access the profits that have accumulated over time and use these funds for their personal lifestyle. One way this can be achieved is declaring and paying dividends.

As with most transactions there are some considerations to keep in mind, particularly when a dividend can be paid and how the disbursement of funds is taxed.

Paying Dividends:

When can I pay the dividend?

As dividends are paid out of Company’s Retained Earnings you will need to confirm that your company has sufficient profits available for distribution as dividends. Your accountant can work with you to devise a dividend payment strategy.

When can I frank the dividend?

Franking credits are the tax payments a company has previously made on the profits. Before you can ‘frank’ a dividend you will need to ensure you understand the following.

- The company must have generated profits and paid corporate tax on those profits before it can frank dividends. Franking is applicable only to profits on which the company has already paid tax.

- Franking Account: You should find a balance of historic tax paid, less any franked distributions as a schedule in your Company’s income tax return. This is a good place to start to gauge how much you may be able to frank a dividend.

- Franking Rate: The franking rate is the proportion of tax paid by the company that can be attached to the dividend. It is expressed as a percentage and typically corresponds to the company’s corporate tax rate. For example, if the company’s tax rate is 25%, the franking rate will be 25%.

The purpose of franking credits is to ensure that the tax already paid by the company is considered when those profits reach the shareholder and to avoid taxing the amount twice.

How Franked dividends work in Australia

- Company Tax Payment: When a company earns profits, it is required to pay income tax on those profits at the applicable tax rate, which is currently 25% for small business entities and 30% for large companies.

- Franking Credits: After paying the income tax, the company receives franking credits, also known as imputation credits, from the Australian Taxation Office (ATO). Franking credits are the amount of tax already paid by the company. This amount is added to the company’s Franking Account so that there is a running tally of franking credits the company can use.

- Dividend Declaration: If the company’s directors decide to distribute profits to shareholders in the form of dividends, they can choose to attach franking credits to the dividend payments. This is known as ‘franking the dividend.’

- Franking Rate: The franking rate is the proportion of the dividend amount that is franked, and it corresponds to the company’s income tax rate. For example, if a company’s tax rate is 25%, the franking rate will be 25%.

Who pays the tax and how much do they pay?

The recipient of the dividend (shareholder) declares the dividend income and pays tax on it.

- Taxation for Shareholders: When a shareholder receives a franked dividend, they include the dividend, including the franking credit amount, in their assessable income for tax purposes. However, they are also entitled to a tax credit for the franking credits attached to the dividend.

- Tax Offset: The tax credit for franking credits is known as a franking credit tax offset. Shareholders can use the franking credits to offset their personal income tax liability, effectively reducing the amount of tax they owe. If the franking credits exceed the tax payable, the excess can be refunded to the shareholder.

- Different Tax Rates for Shareholders: Shareholders may have different tax rates based on their personal circumstances. The benefit of franking credits varies depending on the individual’s tax rate. Some shareholders may receive a refund, while others may have tax payable.

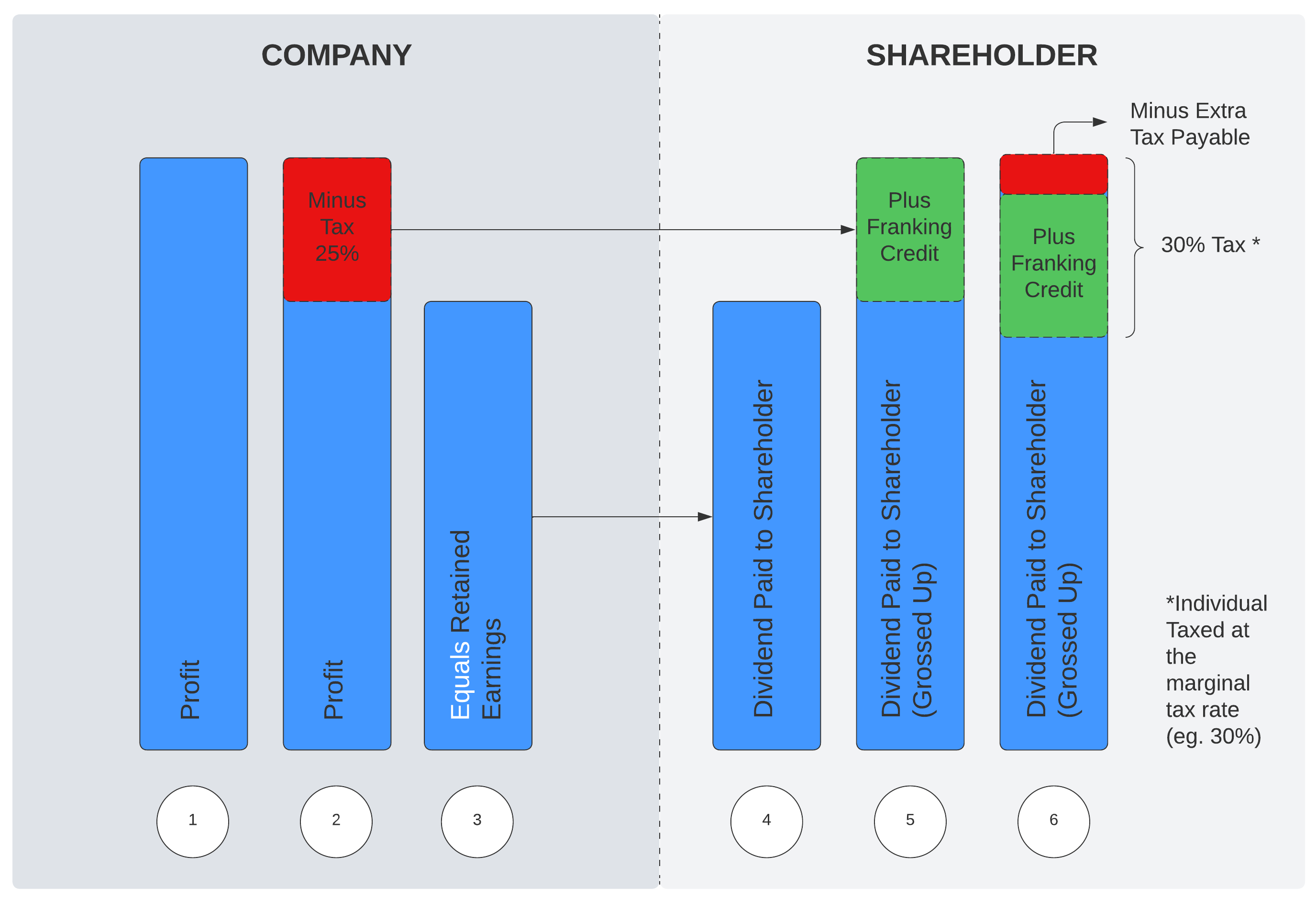

Steps illustrated:

- Company makes a tax profit for the year

- Company pays tax – 25% tax rate for small businesses

- Company has profit after tax (this is called “retained earnings”)

- Company uses retained earnings to pay a dividend to shareholder (shareholder receives this amount as cash payment)

- Shareholder’s taxable income is “grossed up” to include the franking credit received on dividend. The franking credit is the tax the company previously paid on profits.

- Shareholder pays tax on “grossed up” amount. If their tax rate is 30% and they received 25% franking credit on dividend, they will need to pay the difference from cash received.

Watch our “How dividends work” video for further clarification.

Case Study

Company ABC is an Australian company that has generated profits and is planning to distribute dividends to its shareholders. The company’s tax rate is 25%, and the directors have decided to issue fully franked dividends. Let’s explore how this scenario would affect two shareholders: Daniel and Katy.

Shareholder Daniel:

- Daniel is an individual shareholder of Company ABC.

- He has other taxable income of 7,000.

- Company ABC declares a fully franked dividend of $7,500 to Daniel.

- The franking rate of 25% attaches $2,500 of franking credits to the dividend. ($7500/75) *25

- Daniel includes the $10,000 dividend in his assessable income for tax purposes. (7500 + 2500) – this is called ‘grossing up’ the dividend and involves adding the cash received and the franking credit together.

- Daniel is entitled to a franking credit tax offset equal to the attached franking credits of $2,500.

- To calculate his tax liability:

- Taxable income: $17,000

- Tax payable: $0

- Less: PAYG Withheld: $0

- Less: Franking credit tax offset: $2,500

- Daniel is entitled to a tax refund of $2,500 after considering the franking credit tax offset.

As Daniel’s total income is under the tax-free threshold, he receives the whole of the franking credits back as a tax refund.

Shareholder Katy:

- Katy is an individual shareholder of Company ABC.

- She has other taxable income of $25,000 from various sources. This attracts tax of $1292.

- Company ABC declares a fully franked dividend of $7,500 to Katy.

- The franking rate is 25%, which means $2,500 of franking credits are attached to the dividend.

- Katy includes the $10,000 dividend in her assessable income for tax purposes.

- Katy is entitled to a franking credit tax offset equal to the attached franking credits of $2,500.

- To calculate her tax liability:

- Taxable income: $35,000

- Tax payable: $3,192

- Less: PAYG Withheld: $1,404

- Less: Franking credit tax offset: $2,500

- Katy’s tax refund is $712 which she is entitled to after considering the franking credit tax offset.

In this case study, both shareholders Daniel and Katy benefit at different levels from the franking credits attached to the dividends they receive. The franking credits attached to Daniel’s dividends have been fully refunded due to his low income. However, for Katy franking credits reduce her tax liability, resulting in lower taxes owed.

Where the average tax rate of the shareholder is above the franking credit rate (normally 25%) it is usual for the shareholder to have to pay ‘top-up’ tax.

Checklist to issue a dividend

- Review Company Constitution: Check the company’s constitution or shareholder agreement to understand any specific provisions or requirements related to dividend payments.

- Hold Directors’ Meeting: As a director of the company, convene a directors’ meeting to propose and declare the dividend. The meeting should be properly documented, and minutes should be kept.

- Decide Dividend Amount: Decide the amount of dividend you wish to pay. This can be a part of the profits or the full amount, depending on your preference and the company’s financial situation.

- Determine the Franking Rate: It is expressed as a percentage and typically corresponds to the company’s corporate tax rate. For example, if the company’s tax rate is 25%, the franking rate will be 25%. When paying franked dividends, it is important to communicate the franking rate and the number of franking credits attached to the dividend to the shareholders.

- Check there are sufficient franking credits in the company’s Franking Account: You need to ensure that the company has enough franking credits to cover the dividend you wish to frank.

- Payable Date and Record Date: Establish a payable date, which is the date when the dividend will be paid to shareholders. Additionally, set a record date, which is the date on which the company will identify the shareholders eligible to receive the dividend. (This is typically used in listed companies where shareholders can change daily – smaller non-listed companies typically record and pay on same date)

- Prepare Dividend Statements: Prepare dividend statements that outline the dividend amount, payable date, and other relevant details. These statements serve as evidence of the dividend payment.

- Include Franking Credits on Dividend Statements: When supplying dividend statements to shareholders, include the franking credits as a separate item. This allows shareholders to easily find the franking credits associated with their dividend income.

- Pay Dividend: Transfer the dividend amount from the company’s bank account to the shareholder’s nominated bank account. Ensure proper documentation of the transaction for record-keeping purposes.

- Reporting and Compliance: Ensure that the company lodges the necessary documentation with the Australian Taxation Office (ATO) to report and verify the franking credits attached to the dividends. Compliance with tax reporting requirements is essential. (For non-listed companies, this forms part of the company tax return)